Why Budgets Fail Even When You Try Hard

If you have ever wondered why budgets fail, the answer usually has less to do with willpower and more to do with the system behind the budget. Most people do not fail because they are lazy or careless. They fail because their budget was never built for real life.

Why Your Budget Keeps Failing (And It’s Not Your Willpower)

One of the biggest reasons why budgets fail is that they are based on an ideal month instead of a real month.

You start the month motivated.

You open your banking app. You promise yourself this month will be different. You will stop overspending. You will finally save money. You will track every purchase, avoid unnecessary takeout, and become the kind of person who always knows where their money is going.

Then life happens.

A car repair shows up. A birthday dinner costs more than expected. Groceries are somehow higher than last week. A subscription renews. One stressful day turns into one delivery order, then two. By the end of the month, the budget is gone, your savings did not grow, and you are left thinking the same painful thought:

“I guess I’m just bad with money.”

But that is usually not true.

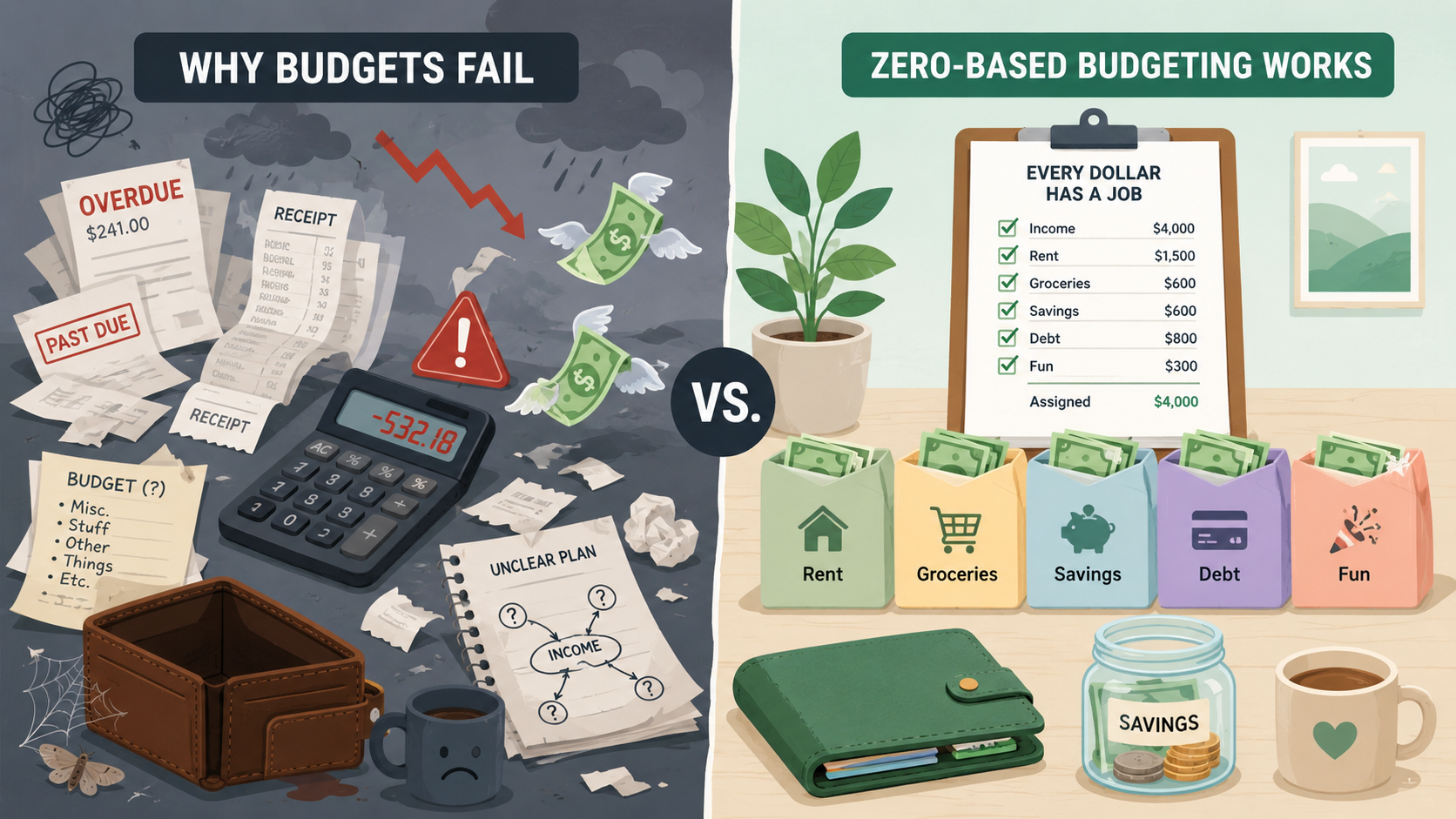

Most budgets do not fail because people are lazy, careless, or weak-willed. They fail because the budget itself was built on a system that could not survive real life.

A good budget is not a guilt spreadsheet. It is not a punishment. It is not a monthly reminder of everything you did wrong.

A good budget is a decision-making system.

And if your budget keeps failing, the problem is probably not your willpower. The problem is that your system is missing one or more of the pieces below.

Your Budget Is Built Around Hope, Not Reality

The most common reason budgets fail is simple: they are based on the month you wish you had, not the month you actually live.

On paper, it is easy to create a perfect budget:

- Groceries: $400

- Eating out: $50

- Entertainment: $25

- Savings: $500

- Miscellaneous: $0

This looks responsible. It also might be completely unrealistic.

If you normally spend $650 on groceries, $250 on restaurants, and $150 on random purchases, a budget that suddenly cuts those categories to almost nothing is not a plan. It is a fantasy.

That does not mean you can never reduce those expenses. It means you need a transition plan, not a financial crash diet.

A realistic budget starts by looking backward before looking forward. Review the last 30 to 90 days of spending. Find your actual averages. Then make small, intentional changes from there.

Instead of saying, “I will only spend $50 eating out this month,” try:

“I usually spend $250 eating out. This month, I will bring it down to $180 and move the extra $70 to savings.”

That is not as dramatic. But it is much more likely to work.

Budgets fail when they ask you to become a completely different person overnight.

Budgets work when they help your current self make better choices one month at a time.

You Forgot About Irregular Expenses

Another reason why budgets fail is that they ignore irregular expenses.

Most people budget for the obvious monthly bills: rent, mortgage, utilities, phone, insurance, groceries, gas, and subscriptions.

Then they get surprised by expenses that were never actually surprises.

Car registration. Holiday gifts. Back-to-school shopping. Annual memberships. Medical appointments. New tires. Wedding travel. Pet care. Home repairs. Tax payments. Birthday gifts.

These expenses do not happen every month, so they are easy to ignore. But they happen eventually, which means they need a place in your budget before they arrive.

This is where many budgets collapse.

You think you have an extra $300 this month. Then an annual bill hits for $240. Suddenly the budget feels broken, even though the expense was predictable.

The solution is to create sinking funds.

A sinking fund is money you set aside gradually for a known future expense. Instead of being surprised by a $600 car repair, you save $50 a month into a car maintenance category. Instead of panicking over December gifts, you save a little every month starting now.

Here are a few sinking fund categories worth considering:

- Car maintenance

- Medical and dental costs

- Holidays and gifts

- Travel

- Home repairs

- Pet care

- Annual subscriptions

- Clothing

- School expenses

- Insurance premiums

A budget that only includes monthly bills is incomplete.

A budget that includes irregular expenses becomes much harder to knock over.

Your Categories Are Too Vague

A category called “miscellaneous” seems harmless.

It is not.

For many people, “miscellaneous” becomes the place where the budget goes to disappear. It starts as a small flexible category, then turns into coffee, Amazon orders, convenience store runs, random fees, birthday cards, batteries, parking, and everything else that does not fit neatly into another box.

The more vague your budget categories are, the less useful your budget becomes.

That does not mean you need 75 categories. Too many categories can make budgeting exhausting. But you do need enough detail to see what is really happening.

For example, instead of one broad “shopping” category, you might separate:

- Household items

- Clothing

- Personal care

- Gifts

- Fun spending

Instead of one “food” category, you might separate:

- Groceries

- Restaurants

- Coffee and snacks

- Delivery apps

This matters because different types of spending require different decisions.

If groceries are high because food prices are rising and your household needs are real, the solution may be meal planning or store swaps. If delivery app spending is high because you are exhausted after work, the solution may be keeping easy backup meals at home.

Specific categories create specific solutions.

Vague categories create vague guilt.

Your Budget Has No Room for Fun

A budget with no fun money is usually a budget waiting to fail.

When people get serious about money, they often cut every enjoyable category first. No restaurants. No hobbies. No coffee. No small treats. No entertainment. No spontaneous plans.

This can work for a short emergency sprint. It rarely works as a long-term lifestyle.

Humans are not machines. If your budget only says “no,” eventually you will stop listening to it.

The goal is not to remove joy from your financial life. The goal is to decide how much joy you can afford on purpose.

That is why guilt-free spending matters.

A realistic budget should include a category for personal spending, fun, or lifestyle choices. The amount will depend on your income, goals, and obligations. But even a small amount can make the budget feel less like a punishment and more like a plan.

For example:

- $25 for coffee or snacks

- $50 for hobbies

- $75 for eating out

- $100 for personal spending

When that money is planned, you can spend it without guilt.

And when it is gone, you know the limit was not random. It was a decision you made ahead of time.

The best budget is not the strictest budget.

The best budget is the one you can actually live with.

You Are Tracking After the Damage Is Done

Many people think budgeting means checking what happened at the end of the month.

But reviewing last month’s spending is not budgeting. It is financial archaeology.

It can teach you something, but it cannot change what already happened.

A working budget needs to guide your decisions while the month is still happening.

That means checking in regularly enough to adjust before things go off track. You do not need to obsess over every transaction, but you do need a rhythm.

Try this simple weekly check-in:

- Look at your account balances.

- Review what you spent this week.

- Check which categories are running low.

- Move money between categories if needed.

- Decide what needs to change next week.

This turns your budget into a living system.

Maybe groceries are higher than expected, so you move money from restaurants. Maybe gas is lower this month, so you send the difference to debt. Maybe you forgot about a birthday, so you reduce entertainment spending for the week.

Adjusting your budget is not failing.

Adjusting your budget is the point.

The Fix: Give Every Dollar a Job

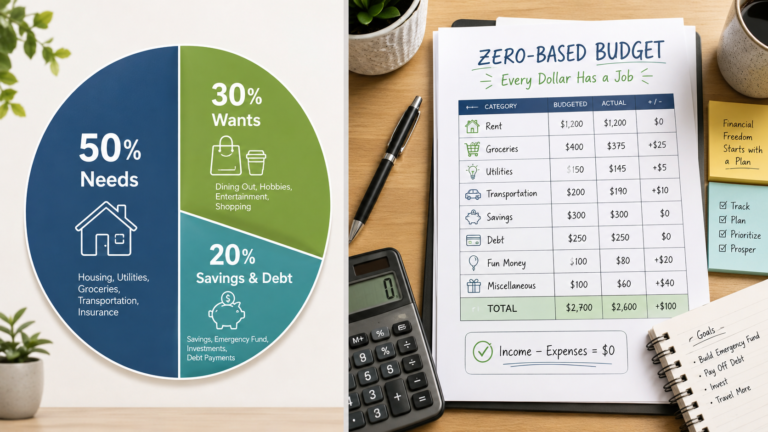

If your budget keeps failing, one of the most useful systems to try is zero-based budgeting.

Zero-based budgeting means every dollar of income gets assigned to a specific job before you spend it.

That job might be rent. Groceries. Debt payoff. Emergency savings. Fun money. Car repairs. Vacation. Giving. Investing. Anything.

The goal is not to have zero dollars in your bank account. The goal is to have zero unassigned dollars in your plan.

Here is a simple example.

Let’s say your monthly take-home pay is $3,500.

You might assign it like this:

| Category | Amount |

|---|---|

| Rent | $1,300 |

| Utilities | $200 |

| Groceries | $450 |

| Transportation | $250 |

| Insurance | $150 |

| Phone | $80 |

| Minimum debt payments | $300 |

| Emergency fund | $250 |

| Car maintenance sinking fund | $100 |

| Medical sinking fund | $75 |

| Eating out | $150 |

| Fun money | $100 |

| Subscriptions | $45 |

| Extra debt payoff | $100 |

| Total assigned | $3,500 |

Every dollar has a job.

This creates clarity. You are no longer hoping there will be money left for savings. You decide at the beginning that savings gets paid. You are no longer surprised by car maintenance. You build it into the plan. You are no longer guessing whether you can afford dinner out. You check the category.

Zero-based budgeting works because it forces tradeoffs into the open.

If you want to spend more on restaurants, the money has to come from somewhere. If you want to save more, another category has to shrink. This is not restriction. This is awareness.

And awareness is where financial control begins.

How to Start This Month

Do not try to build the perfect budget on your first attempt.

Start with a simple reset.

Step 1: Find your real income

Use your actual take-home pay after taxes and deductions. If your income changes month to month, start with a conservative estimate.

Step 2: List your fixed bills

Write down the expenses that are predictable and required: housing, utilities, insurance, debt minimums, subscriptions, childcare, transportation, and other essentials.

Step 3: Estimate flexible spending

Look at groceries, restaurants, gas, shopping, entertainment, and personal spending. Use real numbers from past months when possible.

Step 4: Add sinking funds

Choose at least three irregular expenses you know will happen. Start small if needed. Even $10 or $25 per category is better than nothing.

Step 5: Assign every dollar

Keep giving your income jobs until your income minus planned expenses equals zero.

Step 6: Check in weekly

Pick one day each week to review and adjust. Put it on your calendar. Treat it like a short meeting with your future self.

A Budget Is Not a Test of Your Character

When a budget fails, it is easy to turn the failure into an identity.

“I’m irresponsible.”

“I’m not disciplined.”

“I’ll never be good with money.”

But a budget is not a test of your character. It is a tool. And when a tool does not work, you do not shame yourself. You improve the tool.

Maybe your categories need more detail. Maybe your food budget is unrealistic. Maybe you need sinking funds. Maybe you need a small fun money category so the plan feels livable. Maybe you need weekly check-ins instead of monthly regret.

None of that means you failed.

It means your system needs better instructions.

Your budget does not need to be perfect. It needs to be honest. It needs to reflect your real life, your real income, your real obligations, and your real priorities.

Start there.

Give every dollar a job.

Then let the budget become what it was always supposed to be:

Not a punishment.

Not a guilt trip.

A plan for building a calmer, more intentional financial life.

Finally, The Consumer Financial Protection Bureau also recommends tracking income and expenses as a first step toward building a realistic budget.

Quick Takeaways

- Budgets often fail because they are unrealistic, incomplete, or too vague.

- Irregular expenses need sinking funds before they become emergencies.

- Fun money is not irresponsible when it is planned.

- A budget should be checked during the month, not only after the month ends.

- Zero-based budgeting helps by giving every dollar a specific job.

- Understanding why budgets fail makes it easier to fix the system without blaming yourself.