50/30/20 vs. Zero-Based: Which Budgeting Method Actually Fits Your Life?

Budgeting advice often sounds simple until you try to apply it to your actual life.

One expert says to use the 50/30/20 rule. Another says to give every dollar a job with zero-based budgeting. Someone else tells you to automate everything and stop thinking about money completely.

So which method is right?

The answer depends on your income, expenses, personality, goals, and how much structure you need.

The 50/30/20 budget vs zero based budgeting comparison is one of the most useful places to start because these two methods solve different problems.

The 50/30/20 budget gives you a simple percentage-based framework.

Zero-based budgeting gives you a detailed dollar-by-dollar plan.

Neither method is automatically better for everyone. The best budget is the one that helps you make better decisions and actually stick with the plan.

This guide breaks down how both methods work, who each method is best for, and how to choose the budgeting system that fits your real life.

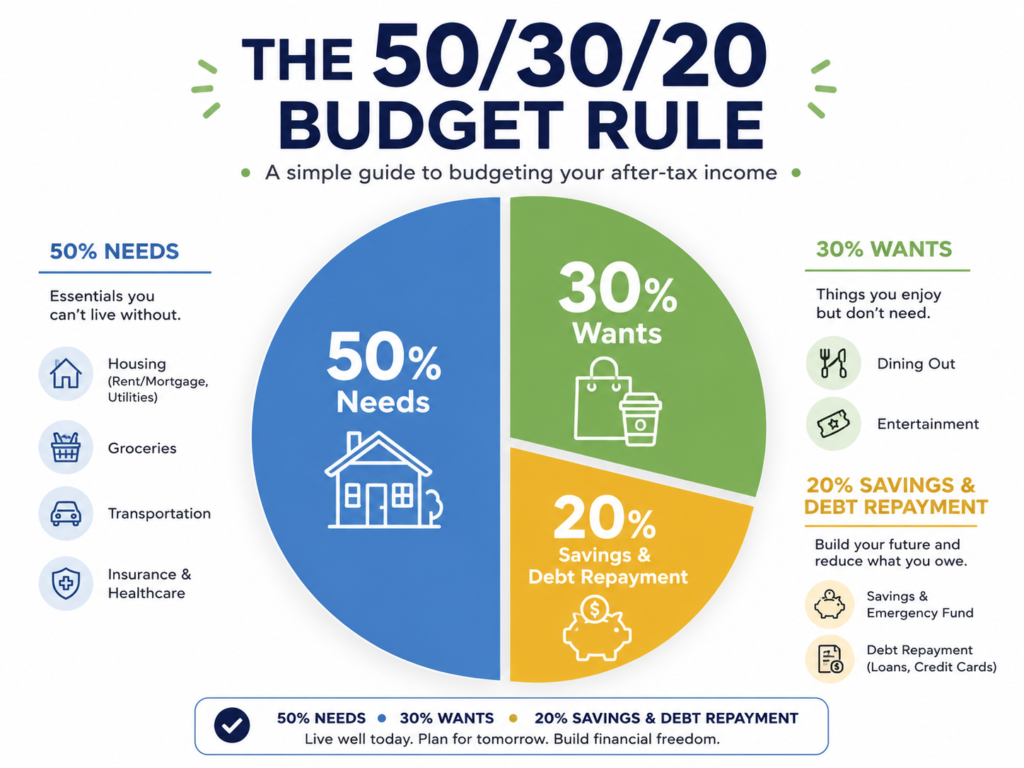

What Is the 50/30/20 Budget?

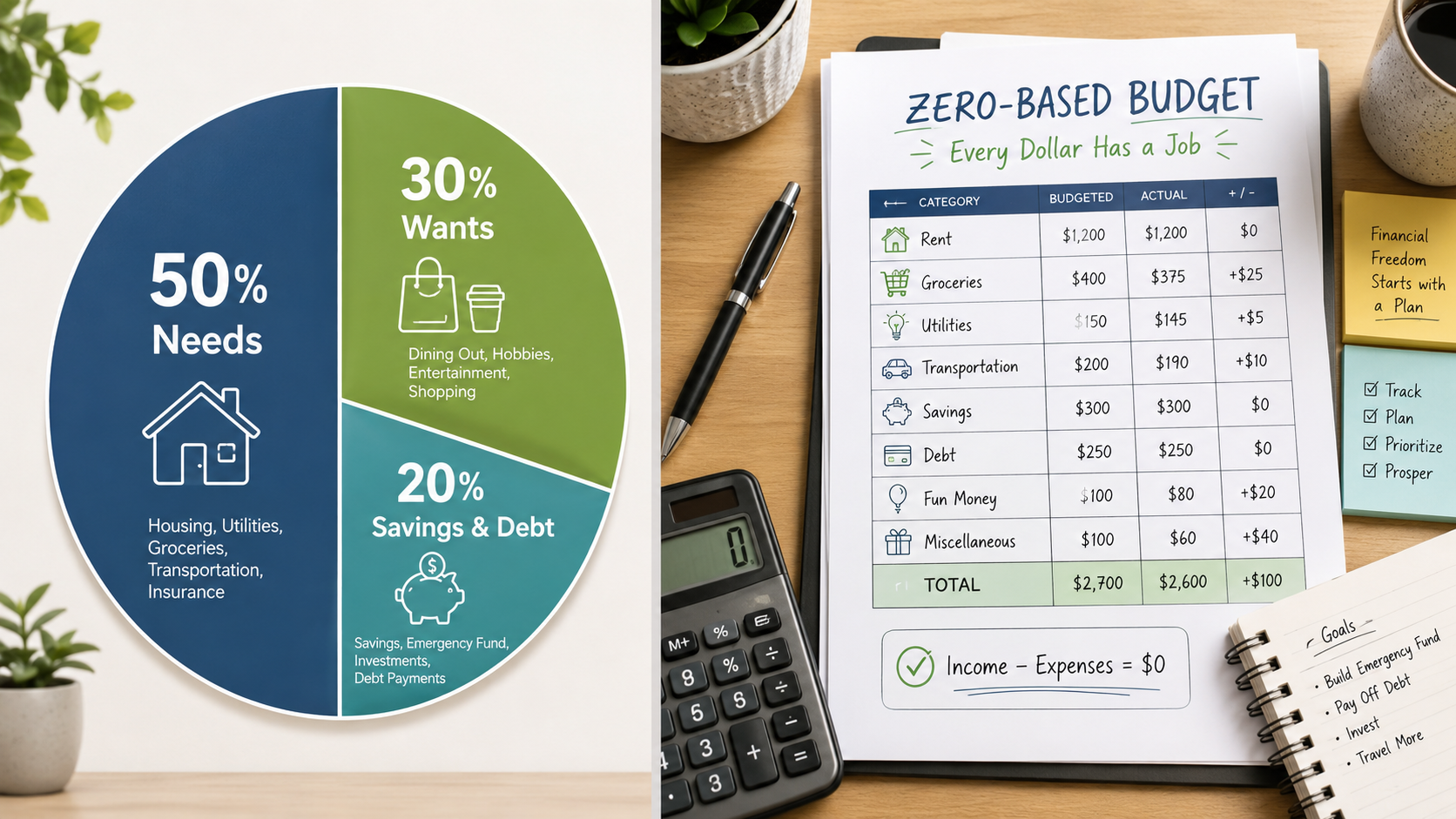

The 50/30/20 budget is a simple budgeting method that divides your after-tax income into three broad categories:

- 50% for needs

- 30% for wants

- 20% for savings and debt repayment

For example, if your monthly take-home pay is $4,000, the 50/30/20 budget would look like this:

| Category | Percentage | Amount |

|---|---|---|

| Needs | 50% | $2,000 |

| Wants | 30% | $1,200 |

| Savings and debt repayment | 20% | $800 |

| Total | 100% | $4,000 |

The appeal is obvious.

It is easy to understand. It does not require dozens of categories. It gives you a quick way to see whether your money is balanced.

Needs usually include things like rent, utilities, groceries, transportation, insurance, childcare, and minimum debt payments.

Wants include restaurants, entertainment, subscriptions, hobbies, shopping, travel, and other lifestyle spending.

Savings and debt repayment include emergency savings, retirement contributions, extra debt payments, investing, sinking funds, and long-term goals.

The 50/30/20 budget works best as a high-level guide.

It helps you answer a simple question:

Is my money generally going in the right direction?

What Is Zero-Based Budgeting?

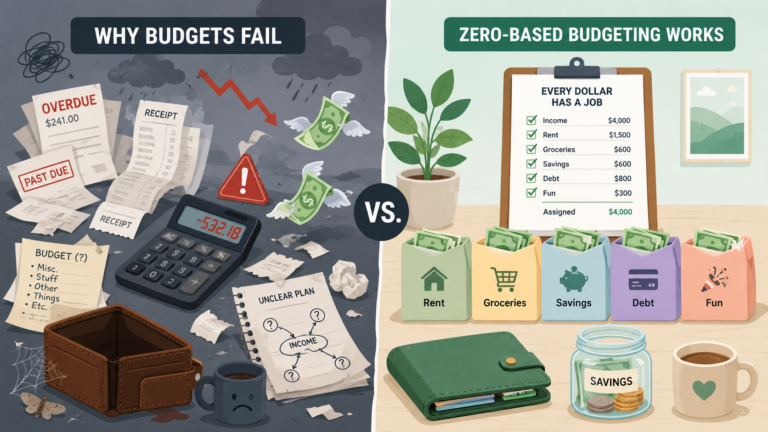

Zero-based budgeting is a budgeting method where every dollar of income is assigned to a specific job.

The formula is:

Income − planned expenses − savings − debt payments = $0 unassigned

This does not mean you spend your bank account down to zero.

It means every dollar has a purpose before the month begins.

For example, if your take-home pay is $4,000, a zero-based budget might look like this:

| Category | Amount |

| Rent | $1,400 |

| Utilities | $250 |

| Groceries | $500 |

| Transportation | $250 |

| Insurance | $180 |

| Phone and internet | $140 |

| Minimum debt payments | $300 |

| Emergency fund | $300 |

| Car maintenance sinking fund | $100 |

| Medical sinking fund | $75 |

| Restaurants | $150 |

| Fun money | $125 |

| Household items | $80 |

| Extra debt payoff | $150 |

| Total assigned | $4,000 |

Zero-based budgeting is more detailed than the 50/30/20 rule.

Instead of saying, “I can spend 50% on needs,” it asks exactly how much you will assign to rent, groceries, transportation, insurance, debt, savings, and every other category.

This makes it especially helpful for people who want more control, have debt, are trying to save aggressively, or feel like money keeps disappearing.

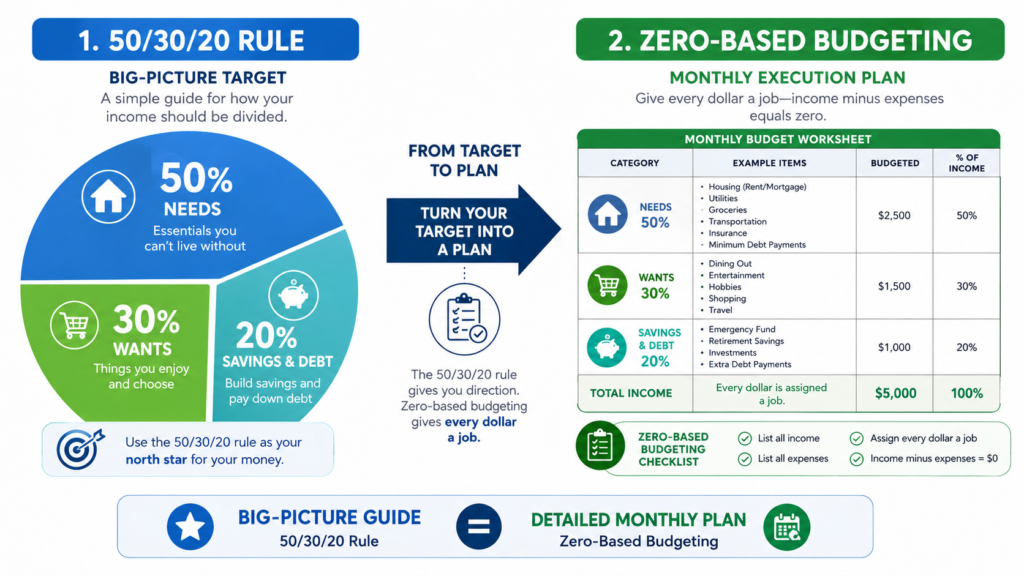

50/30/20 Budget vs Zero Based Budgeting: The Core Difference

The biggest difference is structure.

The 50/30/20 rule is a percentage framework.

Zero-based budgeting is an assignment system.

The 50/30/20 budget tells you the general shape of your financial life. Zero-based budgeting tells every dollar where to go.

Think of the 50/30/20 budget like a map of the city.

Think of zero-based budgeting like turn-by-turn directions.

Both can be useful. But they are useful in different situations.

If your finances are already stable and you mostly need a quick check, the 50/30/20 rule may be enough.

If your money feels chaotic or you need to hit specific goals, zero-based budgeting may work better.

The 50/30/20 budget vs zero based budgeting decision is really a question of how much detail you need to feel in control.

Difference 1: Simplicity vs. Precision

The 50/30/20 budget is easier to start.

You only need three major categories. That makes it less intimidating for beginners who do not want to track every small purchase.

This simplicity is its biggest strength.

But it is also its biggest weakness.

Three categories may be too broad if you need to understand where your money is actually going.

For example, your “wants” category might include restaurants, subscriptions, clothes, coffee, entertainment, and travel. If you overspend, the method may not immediately show which habit caused the problem.

Zero-based budgeting gives more precision.

Instead of one large “wants” bucket, you can create separate categories for restaurants, fun money, subscriptions, gifts, clothing, and hobbies.

That detail makes it easier to solve specific problems.

If your goal is simplicity, the 50/30/20 budget wins.

If your goal is precision, zero-based budgeting wins.

Difference 2: Flexibility vs. Control

The 50/30/20 budget is flexible because it does not require you to plan every dollar in advance.

As long as your spending stays within the broad percentages, you are technically on track.

This can feel freeing.

But if you struggle with overspending, too much flexibility can become a problem.

Zero-based budgeting gives more control because every dollar is assigned ahead of time.

You know how much is for groceries, how much is for gas, how much is for savings, and how much is for fun.

This can reduce decision fatigue because the plan already exists.

The tradeoff is that zero-based budgeting requires more maintenance. You need to review categories, update spending, and adjust when real life changes.

If you want a loose structure, the 50/30/20 budget may feel better.

If you want a clear monthly plan, zero-based budgeting may be stronger.

Difference 3: Best for Stable Finances vs. Best for Financial Change

The 50/30/20 budget works well when your finances are already fairly stable.

It can help you maintain balance and avoid lifestyle creep.

But if you are trying to make a major financial change, it may not be detailed enough.

Zero-based budgeting is especially useful when you are trying to:

- Pay off debt

- Build an emergency fund

- Save for a major goal

- Stop overdrafting

- Reduce overspending

- Prepare for irregular expenses

- Track multiple priorities at once

Why?

Because change requires specificity.

If you want to pay off debt faster, you need to know exactly how much extra you can send this month. If you want to build savings, you need to assign savings before the money disappears. If you want to stop overspending on restaurants, you need a restaurant category.

The 50/30/20 rule helps you see the big picture.

Zero-based budgeting helps you change the details.

Difference 4: How Each Method Handles Debt

Debt is where the two methods can feel very different.

In the 50/30/20 budget, minimum debt payments usually count as needs because they are required bills. Extra debt payments usually go into the 20% savings and debt repayment category.

That works fine if your debt is manageable.

But if you have high-interest credit card debt or multiple loans, the 50/30/20 structure may not be aggressive enough.

Zero-based budgeting lets you build debt payoff directly into the plan.

You can assign money to:

- Minimum payments

- Extra credit card payments

- Debt avalanche strategy

- Debt snowball strategy

- A buffer to avoid adding new debt

This makes debt payoff more intentional.

For someone with serious debt goals, zero-based budgeting often works better because it gives every extra dollar a clear job.

The 50/30/20 budget can show that debt payoff matters.

Zero-based budgeting can show exactly how it will happen.

Difference 5: How Each Method Handles Irregular Expenses

Irregular expenses are one of the biggest reasons budgets fail.

These include things like:

- Car repairs

- Annual subscriptions

- Holiday gifts

- Medical bills

- Insurance premiums

- School expenses

- Pet care

- Travel

- Home repairs

The 50/30/20 budget can include these expenses, but it does not automatically show where to put them.

They may fit under needs, wants, or savings depending on the situation.

Zero-based budgeting handles irregular expenses more clearly through sinking funds.

A sinking fund is money you set aside gradually for a future expense.

For example:

| Future Expense | Estimated Annual Cost | Monthly Sinking Fund |

| Car maintenance | $900 | $75 |

| Holiday gifts | $600 | $50 |

| Medical expenses | $720 | $60 |

| Annual subscriptions | $240 | $20 |

Instead of being surprised by a $600 bill, you prepare for it little by little.

This is one of the strongest advantages of zero-based budgeting.

If irregular expenses keep knocking your budget off track, zero-based budgeting may be the better fit.

Difference 6: How Each Method Handles Fun Money

A good budget needs room for real life.

The 50/30/20 budget does this well because it gives wants an official place in the plan.

That can reduce guilt.

When 30% is assigned to wants, spending on restaurants, hobbies, entertainment, or travel does not feel like failure. It is part of the framework.

Zero-based budgeting also allows fun money, but it requires you to choose the exact amount.

This can be helpful if you tend to overspend in lifestyle categories.

For example, instead of one broad wants category, you might assign:

| Fun Category | Amount |

| Restaurants | $150 |

| Coffee and snacks | $40 |

| Hobbies | $75 |

| Entertainment | $60 |

| Personal spending | $100 |

This makes fun spending intentional.

The 50/30/20 budget gives you permission.

Zero-based budgeting gives you boundaries.

Both are useful. The right choice depends on whether your fun spending needs freedom or limits.

Difference 7: Time Required

The 50/30/20 budget is faster.

You can set it up quickly and review it occasionally.

That makes it a good option for people who want a simple financial checkup without managing many categories.

Zero-based budgeting takes more time.

You need to create categories, assign money, track spending, and adjust during the month.

But the extra time can be worth it if your finances need more attention.

A good way to think about it:

The 50/30/20 budget is lower effort and lower detail.

Zero-based budgeting is higher effort and higher control.

If you are overwhelmed, start with the 50/30/20 rule.

If you are frustrated because money keeps slipping away, try zero-based budgeting.

Example 1: The 50/30/20 Budget for a $4,000 Income

Let’s say your monthly take-home pay is $4,000.

Under the 50/30/20 rule:

| Category | Amount |

| Needs | $2,000 |

| Wants | $1,200 |

| Savings and debt repayment | $800 |

| Total | $4,000 |

This is clean and simple.

But what if your rent alone is $1,600? What if your car payment, insurance, utilities, groceries, and gas push needs to $2,700?

Then the 50/30/20 rule may not fit perfectly.

That does not mean you failed. It means the framework needs to be adjusted for your real life.

Percentages are guidelines, not laws.

Example 2: Zero-Based Budget for a $4,000 Income

Here is the same $4,000 income using zero-based budgeting:

| Category | Amount |

| Rent | $1,500 |

| Utilities | $250 |

| Groceries | $500 |

| Transportation | $250 |

| Insurance | $180 |

| Phone and internet | $140 |

| Minimum debt payments | $300 |

| Emergency fund | $250 |

| Extra debt payoff | $200 |

| Car maintenance | $100 |

| Medical sinking fund | $75 |

| Restaurants | $125 |

| Fun money | $80 |

| Household items | $50 |

| Miscellaneous buffer | $0 |

| Total assigned | $4,000 |

This method shows exactly where the money goes.

It also makes tradeoffs more visible.

If you want more fun money, it has to come from somewhere. If you want more savings, another category has to shrink.

That is not a bad thing.

That is what budgeting is: choosing on purpose.

Which Budgeting Method Fits Your Life?

Use the 50/30/20 budget if:

- You want something simple

- Your finances are fairly stable

- You do not want many categories

- You need a quick spending check

- You are not aggressively paying off debt

- You like flexible guidelines

Use zero-based budgeting if:

- You want more control

- You are paying off debt

- You are building savings

- You have irregular expenses

- You often wonder where your money went

- You need clear category limits

- You want every dollar assigned before the month begins

The 50/30/20 budget vs zero based budgeting choice does not have to be permanent.

You can start with one and switch later.

You can even combine both.

How to Combine the 50/30/20 Rule and Zero-Based Budgeting

For many people, the best answer is not either/or.

It is both.

You can use the 50/30/20 rule as your big-picture target and zero-based budgeting as your monthly execution plan.

Here is how:

- Start with your income.

- Use 50/30/20 as a general benchmark.

- Create detailed zero-based categories.

- Assign every dollar.

- Compare your final budget to the 50/30/20 percentages.

- Adjust over time.

For example, maybe your current budget is:

- 62% needs

- 18% wants

- 20% savings and debt

That may not be ideal long term, but it gives you information.

If housing or debt is pushing needs too high, you can make a plan. If wants are too high, you can set better limits. If savings are too low, you can gradually increase them.

The 50/30/20 rule gives the big picture.

Zero-based budgeting gives the action plan.

Together, they can be powerful.

Common Mistakes to Avoid

Mistake 1: Treating Percentages Like Moral Rules

If your budget does not fit 50/30/20 perfectly, that does not mean you are bad with money.

High rent, childcare, medical costs, debt, location, and income all affect what is realistic.

Use percentages as a guide, not a judgment.

Mistake 2: Making Zero-Based Budgeting Too Complicated

You do not need 60 categories to start.

Begin with the categories that matter most. Add more detail only where you need it.

Mistake 3: Forgetting Savings in Both Methods

Savings should not be whatever is left at the end.

Whether you use 50/30/20 or zero-based budgeting, pay your future self on purpose.

Mistake 4: Ignoring Real Spending History

A budget built on fantasy will fail.

Before choosing numbers, review what you actually spent over the last few months.

Mistake 5: Never Adjusting

Your budget should change when your life changes.

A good budget is not frozen. It is reviewed, adjusted, and improved.

The Bottom Line

The 50/30/20 budget and zero-based budgeting are both useful, but they serve different needs.

The 50/30/20 budget is simple, flexible, and great for a quick financial checkup.

Zero-based budgeting is detailed, intentional, and better for people who want stronger control over spending, saving, debt payoff, and irregular expenses.

The best method is not the one that sounds smartest.

The best method is the one you will actually use.

If you need simplicity, start with 50/30/20.

If you need clarity, start with zero-based budgeting.

If you want both, use 50/30/20 as your target and zero-based budgeting as your plan.

Your budget should fit your life, not the other way around.

you can use saving and investing calculators here

Quick Takeaways

- The 50/30/20 budget divides income into needs, wants, and savings or debt repayment.

- Zero-based budgeting assigns every dollar to a specific job.

- The 50/30/20 rule is simpler, but zero-based budgeting is more precise.

- Zero-based budgeting is often better for debt payoff, savings goals, and irregular expenses.

- The 50/30/20 rule can still be useful as a big-picture benchmark.

- You can combine both methods for a balanced and practical budgeting system.

Why Your Budget Keeps Failing (And It’s Not Your Willpower)

The Zero-Based Budget: A Beginner’s Blueprint for Every Dollar