7 Steps to Zero-Based Budgeting for Beginners

The Zero-Based Budget: A Beginner’s Blueprint for Every Dollar

If money keeps disappearing before the end of the month, you do not need a more complicated budget.

You need a clearer one.

That is where zero-based budgeting for beginners can help. Instead of guessing where your money went after it is already gone, zero-based budgeting gives every dollar a job before you spend it.

The idea is simple:

Income minus planned expenses equals zero.

That does not mean you spend every dollar until your bank account hits zero. It means every dollar is assigned to a purpose: bills, groceries, savings, debt, fun, investing, emergencies, or future expenses.

A zero-based budget helps you stop asking, “Where did my money go?” and start saying, “Here is where my money is going.”

This beginner-friendly guide will show you how the system works, how to set it up, and how to use it without feeling overwhelmed.

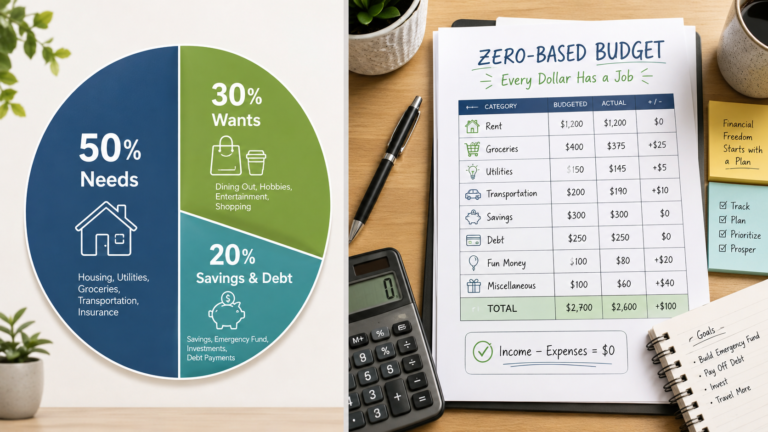

What Is Zero-Based Budgeting?

Zero-based budgeting is a budgeting method where you assign every dollar of income to a specific category until there is no money left unplanned.

The formula looks like this:

Monthly income − monthly expenses − savings − debt payments − giving − fun money = $0

Again, the goal is not to empty your bank account. The goal is to avoid leaving money without a purpose.

For example, if you bring home $4,000 this month, your budget should assign the full $4,000.

Some of it may go to rent. Some to groceries. Some to savings. Some to debt. Some to fun. Some to sinking funds for future expenses.

At the end, your plan should equal your income.

That is why zero-based budgeting for beginners is so powerful: it turns budgeting from a vague tracking habit into a clear decision-making system.

If you are new to budgeting, the Consumer Financial Protection Bureau recommends starting by tracking your income and expenses so you can build a realistic monthly plan.

Why Zero-Based Budgeting Works

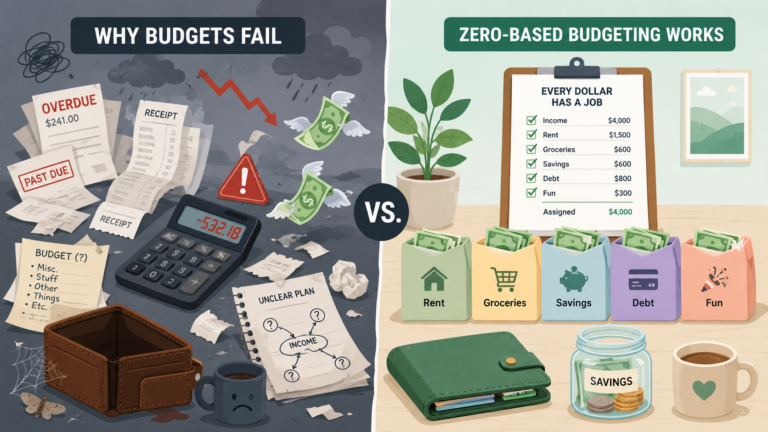

Many budgets fail because they only track spending after it happens.

That can be useful, but it is not enough.

Tracking tells you what happened. Budgeting helps you decide what should happen next.

Zero-based budgeting works because it forces you to make those decisions before the month begins.

Instead of hoping you will have money left to save, you assign money to savings first.

Instead of being surprised by irregular expenses, you create categories for them ahead of time.

Instead of feeling guilty about spending, you create realistic limits for the things you actually value.

This system works especially well if you want to:

- Stop overspending

- Build an emergency fund

- Pay off debt

- Save for future expenses

- Understand where your money is going

- Feel more in control of your finances

- Reduce money stress

Zero-based budgeting is not about being strict for the sake of being strict. It is about being intentional.

Step 1: Calculate Your Monthly Take-Home Income

The first step is to know exactly how much money you have to work with.

Use your take-home income, not your gross salary. That means the amount that actually lands in your bank account after taxes, insurance, retirement contributions, and other deductions.

If you are paid a fixed salary, this step is simple. Add up your paychecks for the month.

If your income changes, use a conservative estimate. Look at your last three to six months of income and choose a number that feels realistic but not overly optimistic.

For example:

| Income Source | Amount |

|---|---|

| Paycheck 1 | $2,000 |

| Paycheck 2 | $2,000 |

| Side income | $300 |

| Total monthly income | $4,300 |

For this example, your zero-based budget starts with $4,300.

That means your job is to assign all $4,300 before the month begins.

Step 2: List Your Fixed Expenses

Fixed expenses are the bills that usually stay the same or close to the same each month.

These are the easiest categories to start with because they are predictable.

Common fixed expenses include:

- Rent or mortgage

- Car payment

- Insurance

- Phone bill

- Internet

- Minimum debt payments

- Subscriptions

- Childcare

- Gym membership

- Utilities, if they are fairly consistent

Here is an example:

| Fixed Expense | Amount |

| Rent | $1,400 |

| Car payment | $350 |

| Insurance | $180 |

| Phone | $80 |

| Internet | $70 |

| Minimum debt payments | $250 |

| Subscriptions | $45 |

| Total fixed expenses | $2,375 |

If your monthly income is $4,300 and your fixed expenses are $2,375, you now have $1,925 left to assign.

This is where many people stop budgeting too early.

But fixed bills are only one part of real life.

Step 3: Plan Your Flexible Spending

Flexible spending includes the categories that change from month to month.

These are often the categories that make or break a budget.

Common flexible expenses include:

- Groceries

- Gas or transportation

- Restaurants

- Coffee and snacks

- Household supplies

- Personal care

- Clothing

- Entertainment

- Fun money

- Gifts

The key is to be realistic.

If you normally spend $700 on groceries, do not suddenly budget $350 and expect it to work perfectly. A budget that ignores your real habits will not survive the month.

Start with your actual spending from the last 30 to 90 days. Then choose a number that improves your habits without creating an impossible plan.

Example:

| Flexible Expense | Amount |

| Groceries | $550 |

| Gas | $220 |

| Restaurants | $150 |

| Household items | $100 |

| Personal care | $75 |

| Fun money | $125 |

| Total flexible spending | $1,220 |

Now your budget has assigned:

- Fixed expenses: $2,375

- Flexible spending: $1,220

- Total assigned so far: $3,595

From your $4,300 income, you still have $705 left to assign.

This is where zero-based budgeting for beginners becomes different from basic expense tracking. You do not just leave that $705 floating around. You give it a job.

Step 4: Add Savings Goals

Savings should not be treated like whatever is left over.

If you wait until the end of the month to save, there may be nothing left.

In a zero-based budget, savings gets planned at the beginning.

Start with your most important savings goal. For many people, that is an emergency fund.

A beginner emergency fund might be $500 or $1,000. After that, you can work toward one month of expenses, then three months, then more depending on your situation.

Savings categories might include:

- Emergency fund

- Vacation

- Home down payment

- New car fund

- Moving fund

- Medical savings

- Investment contributions

- Holiday savings

Example:

| Savings Goal | Amount |

| Emergency fund | $300 |

| Vacation fund | $100 |

| Holiday fund | $50 |

| Total savings | $450 |

Now your total assigned is:

- Fixed expenses: $2,375

- Flexible spending: $1,220

- Savings: $450

- Total assigned: $4,045

You still have $255 left to assign.

Step 5: Create Sinking Funds for Irregular Expenses

Sinking funds are one of the biggest reasons zero-based budgeting works.

A sinking fund is money you set aside slowly for expenses that are predictable but not monthly.

These expenses often feel like emergencies only because they were not planned for.

Examples include:

- Car repairs

- Car registration

- Annual subscriptions

- Medical bills

- Dental visits

- Holiday gifts

- Birthday gifts

- School supplies

- Pet expenses

- Home repairs

- Travel

Let’s say you expect to spend $600 on car maintenance over the next year. Instead of waiting until something breaks, you can save $50 per month.

That turns a future financial shock into a normal monthly category.

Example sinking funds:

| Sinking Fund | Monthly Amount |

| Car maintenance | $75 |

| Medical expenses | $50 |

| Gifts | $40 |

| Total sinking funds | $165 |

Now your budget looks like this:

| Category Group | Amount |

| Fixed expenses | $2,375 |

| Flexible spending | $1,220 |

| Savings | $450 |

| Sinking funds | $165 |

| Total assigned | $4,210 |

You still have $90 left to assign.

Step 6: Assign the Remaining Money

At this point, you keep assigning money until the budget reaches zero unassigned dollars.

You could put the remaining $90 toward:

- Extra debt payoff

- Emergency savings

- Investing

- Groceries

- Fun money

- Giving

- A sinking fund

There is no single correct answer. The best choice depends on your goals.

If you are behind on bills, assign it to bills.

If you have high-interest debt, assign it to debt.

If you have no emergency fund, assign it to savings.

If your budget is too tight and unrealistic, assign some to fun or flexible spending so you can actually stick with the plan.

Here is the final example:

| Category Group | Amount |

| Fixed expenses | $2,375 |

| Flexible spending | $1,220 |

| Savings | $450 |

| Sinking funds | $165 |

| Extra debt payoff | $90 |

| Total assigned | $4,300 |

| Income | $4,300 |

| Unassigned money | $0 |

That is a zero-based budget.

Every dollar has a job.

Step 7: Track and Adjust During the Month

The budget you create at the beginning of the month is a plan, not a prison.

Real life will change.

Groceries may cost more than expected. Gas may be lower than usual. A friend may invite you to dinner. A bill may be higher than planned.

That does not mean the budget failed.

It means you need to adjust.

A weekly budget check-in can keep the system working.

During your check-in, ask:

- How much did I spend this week?

- Which categories are getting low?

- Did any surprise expenses come up?

- Do I need to move money between categories?

- Am I still on track with savings and debt goals?

For example, if restaurants are running high, you might move $40 from fun money. If groceries are lower than expected, you might move the extra money to savings.

The rule is simple:

Move money intentionally before you overspend accidentally.

This is how zero-based budgeting becomes flexible instead of stressful.

Zero-Based Budgeting Example for Beginners

Here is a complete beginner example using a $4,000 monthly income.

| Category | Amount |

| Rent | $1,400 |

| Utilities | $250 |

| Groceries | $500 |

| Transportation | $250 |

| Insurance | $180 |

| Phone and internet | $140 |

| Minimum debt payments | $300 |

| Emergency fund | $300 |

| Car maintenance sinking fund | $100 |

| Medical sinking fund | $75 |

| Gifts sinking fund | $50 |

| Restaurants | $150 |

| Fun money | $125 |

| Household items | $80 |

| Extra debt payoff | $100 |

| Total assigned | $4,000 |

This budget is not perfect for everyone. That is the point.

Your budget should match your income, your bills, your priorities, and your real life.

Zero-based budgeting for beginners is not about copying someone else’s numbers. It is about learning how to make every dollar support your own goals.

Common Zero-Based Budgeting Mistakes

Zero-based budgeting is simple, but beginners often make a few common mistakes.

Mistake 1: Making the Budget Too Strict

If your budget has no room for fun, flexibility, or small surprises, it will probably break.

Do not create a budget for your most disciplined self. Create a budget for your real self.

Mistake 2: Forgetting Irregular Expenses

If you do not plan for car repairs, gifts, medical bills, and annual expenses, they will keep feeling like emergencies.

Sinking funds solve this problem.

Mistake 3: Using Too Many Categories

A category for every tiny purchase can make budgeting exhausting.

Start with simple categories. Add detail only where you need more control.

Mistake 4: Not Checking In

A zero-based budget needs attention during the month.

You do not need to check it five times a day, but a weekly review can prevent small problems from becoming big ones.

Mistake 5: Thinking Adjustments Mean Failure

Changing the budget during the month is not cheating.

It is budgeting.

The goal is not to predict everything perfectly. The goal is to stay intentional when things change.

Best Categories for a Beginner Zero-Based Budget

If you are not sure where to start, use these basic category groups:

Needs

- Housing

- Utilities

- Groceries

- Transportation

- Insurance

- Minimum debt payments

- Childcare

Goals

- Emergency fund

- Extra debt payoff

- Investing

- Retirement

- Down payment

- Education savings

Sinking Funds

- Car maintenance

- Medical expenses

- Gifts

- Holidays

- Travel

- Annual bills

- Pet care

Lifestyle

- Restaurants

- Fun money

- Hobbies

- Clothing

- Personal care

- Subscriptions

This structure gives you enough detail to make good decisions without making the budget too complicated.

Is Zero-Based Budgeting Right for You?

Zero-based budgeting may be a good fit if you like clarity and want to feel more in control of your money.

It is especially helpful if:

- You often wonder where your money went

- You struggle to save consistently

- You are paying off debt

- You have irregular expenses

- You want a more hands-on budgeting system

- You need a clear monthly plan

It may not be the best fit if you prefer a very loose budget or do not want to check in regularly.

But even then, you can use a simplified version.

You do not have to budget every dollar into 40 categories. You can start with a few big categories and build from there.

The best budget is not the most detailed one.

The best budget is the one you will actually use.

How to Start Your First Zero-Based Budget Today

Here is the simplest way to begin:

- Write down your monthly take-home income.

- List your fixed bills.

- Estimate your flexible spending.

- Add savings goals.

- Add sinking funds.

- Assign every remaining dollar.

- Check in once a week.

Do not worry about getting it perfect.

Your first zero-based budget will probably need changes. That is normal. The first month teaches you what your real categories should be. The second month gets easier. By the third month, you will start seeing patterns clearly.

Budgeting is not about controlling every penny forever.

It is about giving yourself a plan, reducing financial surprises, and making your money match your priorities.

With zero-based budgeting, every dollar has a job.

And when every dollar has a job, your money finally starts working with you instead of disappearing on you.

Quick Takeaways

- Zero-based budgeting means assigning every dollar of income to a specific purpose.

- The goal is not to spend everything. The goal is to leave no money unplanned.

- Beginners should start with income, fixed expenses, flexible spending, savings, and sinking funds.

- Sinking funds help prevent predictable expenses from becoming emergencies.

- Weekly check-ins make the budget flexible and realistic.

- Zero-based budgeting for beginners works best when the plan is honest, simple, and built for real life.